In nearly all revocable living trusts the Grantor of the trust is also the primary beneficiary of the trust. An individual nominated as a trustee holds the right to decline the appointment or drop the role completely.

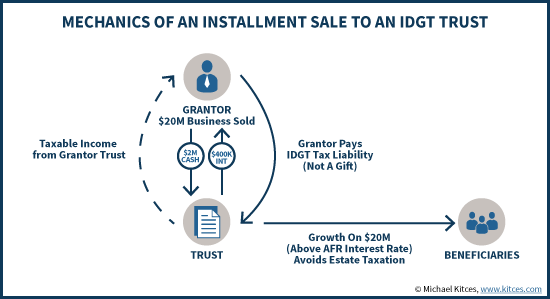

Installment Sale To An Idgt To Reduce Estate Taxes

Installment Sale To An Idgt To Reduce Estate Taxes

After a deed is recorded the grantee owns the property.

Who is the grantor of a trust. The grantor is the owner or seller of the real estate. With this type of structure the income from the trust is taxed to the grantor not the trust itself. A grantor trust is a trust in which the individual who creates the trust is the owner of the assets and property for income and estate tax purposes.

Executor is the person appointed by the grantor to take charge of managing the trust. Additionally the grantor is responsible for informing the. The person establishing the trust retains control over trusts income and assets.

Examples of powers that will cause a trust to be treated as a Grantor Trust include some of the following. The person who creates a trust is always called the grantor regardless of whether he creates a grantor trust or a different type of trust. The grantee is the person or buyer receiving the deed.

A Deed of Trust is a third-party instrument used to create voluntary liens in real estate. Most grantor trusts have both trustees and successor trustees. Can a Grantor of a Trust also be a Beneficiary.

The parties to a Deed of Trust are the Grantor who is the property owner the Beneficiary who is the lender and the Public Trustee who holds certain powers of foreclosure and release. Children or other named successor beneficiaries only benefit from trust assets after the death of the Grantor. A grantor is the entity that establishes a trust and legally transfers control of those assets to a trustee who manages it for one or more beneficiaries.

For a grantor trust the grantor is usually also a trustee and beneficiary of the trusts income and principal. Certain powers reserved by the Grantor in the trust agreement will cause a trust to be treated as a Grantor Trust for tax purposes. In this case all of the termssettlor trustor grantor and trusteerefer to the same person.

In other words the Grantor of a Trust contract is the owner of the asset s which could be any asset from personal residential real estate to stock accounts to business or partnership assets and anything else of monetary value. A deed of trust has three parties known as the grantor trustee and lender or beneficiary. The trustee is the person tasked with managing the trusts assets.

The Grantor in a Trust is the person with the bucks. What is a Grantor Trust. The grantor is sometimes also called the trustor or the settlor.

Through the grantors life and through the life of the trust the trust grantor remains in control of the assets placed in the trust. A grantor trust is the legal entity a person creates whereas the grantor of a trust is the person who creates it. A trustee can be just one person or a group of people.

The trustee is the individual charged with managing the trust. The grantor can add and remove assets and is also entitled to the income and principal of the trust. Often the trust-maker of a revocable living trust will appoint themselves as the trustee the handler of the trust of their own trust.

In most cases the person who funds the trust is identified in the trust agreement as the person who created the trust ie. In grantor trusts the grantor retains certain powers over the trust administration. The person who creates the living trust.

These powers include the power to revoke amend or terminate the trust. Internal Revenue Code Sections 673-678 set forth the rules for determining when the grantor and in some cases another person is treated as the owner of any portion of the trust. Because of these basic principles the Internal Revenue Service IRS taxes the grantor on the trusts income.

Because the trust is revocable ie can be changed or terminated until the grantor dies the grantor can change any part of the trust as often as he or she likes. According to the IRS a grantor trust is one in which the grantor ie. Prior to death the person holding the role of grantor in a grantor trust retains full control of whatever property is in the trust and holds the ability to terminate the trust or change the terms at will.

The grantor of a trust is the person who provides the property or other funds to the trust that becomes the trust corpus assets. What Makes a Trust a Grantor Trust. He or she decides what property to include and who the beneficiaries will be.

The grantor also keeps control over the property inside the trust. A grantor trust is a type of living trust which means it takes effect during the lifetime of the individual who created it. In fact in the context of a revocable living trust the person establishing a trust is usually the Grantor the Initial Trustee and the primary Beneficiary of the trust all at the same time.

For example the grantor in such a trust maintains the ability to make changes or amendments to the trust and to revoke or terminate the trust. In a grantor trust the grantor keeps certain powers over administration of the trust as well as the assets inside the trust. A grantor is sometimes known as the settlor or donor of the trust.

In many revocable living trusts the grantor takes on the role of trustee during their lifetime. It is the person who funds the trust. Grantor trust rules are the rules that apply to.

When the grantor dies the trust automatically turns into a non-grantor trust. In certain types of trusts the grantor.