In nearly all revocable living trusts the Grantor of the trust is also the primary beneficiary of the trust. An individual nominated as a trustee holds the right to decline the appointment or drop the role completely.

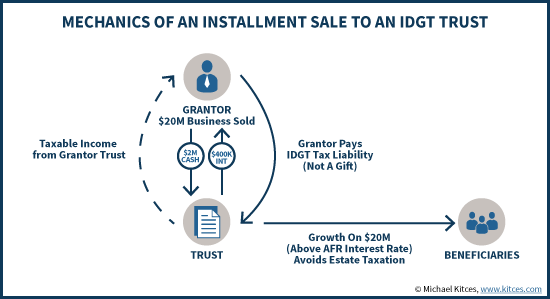

Installment Sale To An Idgt To Reduce Estate Taxes

Installment Sale To An Idgt To Reduce Estate Taxes

After a deed is recorded the grantee owns the property.

Who is the grantor of a trust. The grantor is the owner or seller of the real estate. With this type of structure the income from the trust is taxed to the grantor not the trust itself. A grantor trust is a trust in which the individual who creates the trust is the owner of the assets and property for income and estate tax purposes.

Executor is the person appointed by the grantor to take charge of managing the trust. Additionally the grantor is responsible for informing the. The person establishing the trust retains control over trusts income and assets.

Examples of powers that will cause a trust to be treated as a Grantor Trust include some of the following. The person who creates a trust is always called the grantor regardless of whether he creates a grantor trust or a different type of trust. The grantee is the person or buyer receiving the deed.

A Deed of Trust is a third-party instrument used to create voluntary liens in real estate. Most grantor trusts have both trustees and successor trustees. Can a Grantor of a Trust also be a Beneficiary.

The parties to a Deed of Trust are the Grantor who is the property owner the Beneficiary who is the lender and the Public Trustee who holds certain powers of foreclosure and release. Children or other named successor beneficiaries only benefit from trust assets after the death of the Grantor. A grantor is the entity that establishes a trust and legally transfers control of those assets to a trustee who manages it for one or more beneficiaries.

For a grantor trust the grantor is usually also a trustee and beneficiary of the trusts income and principal. Certain powers reserved by the Grantor in the trust agreement will cause a trust to be treated as a Grantor Trust for tax purposes. In this case all of the termssettlor trustor grantor and trusteerefer to the same person.

In other words the Grantor of a Trust contract is the owner of the asset s which could be any asset from personal residential real estate to stock accounts to business or partnership assets and anything else of monetary value. A deed of trust has three parties known as the grantor trustee and lender or beneficiary. The trustee is the person tasked with managing the trusts assets.

The Grantor in a Trust is the person with the bucks. What is a Grantor Trust. The grantor is sometimes also called the trustor or the settlor.

Through the grantors life and through the life of the trust the trust grantor remains in control of the assets placed in the trust. A grantor trust is the legal entity a person creates whereas the grantor of a trust is the person who creates it. A trustee can be just one person or a group of people.

The trustee is the individual charged with managing the trust. The grantor can add and remove assets and is also entitled to the income and principal of the trust. Often the trust-maker of a revocable living trust will appoint themselves as the trustee the handler of the trust of their own trust.

In most cases the person who funds the trust is identified in the trust agreement as the person who created the trust ie. In grantor trusts the grantor retains certain powers over the trust administration. The person who creates the living trust.

These powers include the power to revoke amend or terminate the trust. Internal Revenue Code Sections 673-678 set forth the rules for determining when the grantor and in some cases another person is treated as the owner of any portion of the trust. Because of these basic principles the Internal Revenue Service IRS taxes the grantor on the trusts income.

Because the trust is revocable ie can be changed or terminated until the grantor dies the grantor can change any part of the trust as often as he or she likes. According to the IRS a grantor trust is one in which the grantor ie. Prior to death the person holding the role of grantor in a grantor trust retains full control of whatever property is in the trust and holds the ability to terminate the trust or change the terms at will.

The grantor of a trust is the person who provides the property or other funds to the trust that becomes the trust corpus assets. What Makes a Trust a Grantor Trust. He or she decides what property to include and who the beneficiaries will be.

The grantor also keeps control over the property inside the trust. A grantor trust is a type of living trust which means it takes effect during the lifetime of the individual who created it. In fact in the context of a revocable living trust the person establishing a trust is usually the Grantor the Initial Trustee and the primary Beneficiary of the trust all at the same time.

For example the grantor in such a trust maintains the ability to make changes or amendments to the trust and to revoke or terminate the trust. In a grantor trust the grantor keeps certain powers over administration of the trust as well as the assets inside the trust. A grantor is sometimes known as the settlor or donor of the trust.

In many revocable living trusts the grantor takes on the role of trustee during their lifetime. It is the person who funds the trust. Grantor trust rules are the rules that apply to.

When the grantor dies the trust automatically turns into a non-grantor trust. In certain types of trusts the grantor.

Trust assets may be included in the trust creators estate when they pass away. As a result the owner of the property has given up their right to the property which is now owned by the trust.

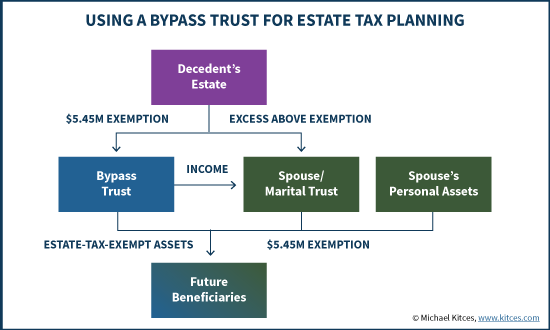

Distributable Net Income Tax Rules For Bypass Trusts

Distributable Net Income Tax Rules For Bypass Trusts

Both types of trust arrangements have advantages and disadvantages.

Grantor trust vs non grantor trust. That is in general a non-grantor trust will be liable for tax on any income including capital gains that it retains while to the extent the non-grantor trust distributes income to its beneficiaries the beneficiaries will be liable instead. Non-grantor trusts are treated as separate entities like a C-Corporation. Under these rules the individual who.

Income earned by a grantor trust is taxed to the settlor. In contrast income earned by a non-grantor trust is generally taxed to the trust unless distributions shift income to beneficiaries. So when looking at the question of what a foreign non-grantor trust is you have to break it down into two parts.

Trusts are legal instruments that can hold and manage assets on behalf of a specified beneficiary named by the original owner of the assets the grantor. This is in comparison to a non-grantor trust in which the original grantor may no longer have control over the trust direct or indirect absent some very creative planning. In a non-grantor trust scenario the trustee will be the only party able to administer the income assets etc.

In estate management a grantor ie. A non-grantor trust also known as an irrevocable trust cannot be revoked unilaterally by the grantor. We will summarize what a Foreign Grantor Trust is.

A non-grantor trust pays income tax at the trust level on any taxable income retained by the trust. A tax identification number for the trust must then be obtained. Because of that theyre treated as if they are direct owners of the trust assets like a sole proprietorship.

If a trust makes a distribution to a beneficiary such distribution will pass the taxable ordinary income but generally not capital gains to the beneficiary to be taxed on the beneficiarys personal income tax return. First of all foreign. A far off Grantor Trust FGT is a sort of trust during which a non-US resident creates a trust for the advantage of beneficiaries living in the country.

In a non-grantor trust scenario the owner of the property in theory at least is no longer deemed the owner of the property and has relinquished control. Definitions A grantor transfers his property to a trust. If you have started the estate planning process youve surely heard of trusts.

A trust is considered foreign if its not a US domestic trust ie. A non-grantor trust also means that this person gives up any right to rescind or amend the trust altogether. The grantor holds the legal authority to transfer property into a trust.

Quite simply a grantor gives up control over all aspects of the trust and its assets. A non-grantor trust on the other hand is recognized as a separate taxable entity. This is determined by a list of powers.

A non-grantor trust pays income tax at the trust level on any taxable income retained by the trust. A grantor will not be treated as the owner of a trust based on a power to affect beneficial enjoyment if the power is exercisable only by Will except for a power to appoint accumulated trust income by Will if the trust provides for the mandatory or discretionary accumulation of trust income by the grantor or a non-adverse party. But grantors of grantor trusts maintain significant rights to the trusts assets and income.

Grantor trusts and intentionally defective grantor trusts become non-grantor trusts at the grantors death. On the flip side a grantor trust allows that person to hold control over the assets and any of its income benefits. Trusts can also be categorized as grantor or non-grantor.

It doesnt meet both the control test where US persons control the substantial decisions of the trust and also doesnt meet the court test where a US court has jurisdiction over the administration of the trust. In a grantor trust the trust creator retains certain powers over the trust including rights to the trusts assets and income. The grantor trust rules are guidelines within the Internal Revenue Code which outline certain tax implications of a grantor trust.

A grantor trust is a trust that can be revoked by the grantor at any time as long as he is alive and mentally competent. The assets held within the trust are then managed by a trustee named by the grantor. A non-US resident is someone who isnt a US citizen isnt a real identification holder and is additionally not considered as a US taxpayer.

If a trust makes a distribution to a beneficiary such distribution will pass the taxable ordinary income but generally not capital gains to the beneficiary to be taxed on the beneficiarys personal income tax return. In some cases a trust can be treated as a grantor trust when a third person nonadverse to the grantor holds an interest or control over the trust that can be attributed to the grantor ex. A grantor trust is any trust in which the grantor is treated as owner of any portion of the trust.

Trustor settlor is the individual who sets up the trust agreement and provides the terms and conditions of the trust. In a non-grantor trust the grantor cannot be named as a trustee beneficiary or a remainderman. A Foreign Grantor Trust is a common type of trust that the grantor controls on behalf of the beneficiary.